President Trump

The trading days leading up to the U.S. presidential election did not feel great. For eight straight trading days, the stock market lost value. It was the first time the market had experienced eight consecutive down days since 2008. Fortunately, this year’s eight-day funk amounted to the S&P 500 losing only about 3% in value. October was a down month for most stock and bond benchmarks, and the consensus view on stocks and the election was that markets liked the certainty that came with a Hillary Clinton presidency (essentially a third term of Obama). Most political analysts and media outlets gave Clinton better grades following the presidential debates, and the trading days following those debates seemed to echo that view. Early polls showed Clinton holding a lead, but the race tightened in the weeks leading up to Election Day.

Nate Silver’s “FiveThirtyEight” website—which performs polling analytics for politics, economics, sports, and other content—had Clinton favored with a 71% probability of winning in the final days prior to the election. Boy, did they get it wrong. There will be countless hours of research that go into studying the 2016 election. FiveThirtyEight aside, many polls showed Donald Trump gaining momentum in late October and early November, and it was that momentum that may have soured the markets. The market didn’t seem to like the “outsider”, a candidate with no political track record and largely undetailed policy ideas. The consensus view held that a Trump election would be followed by a market sell-off, and the comparison to a Brexit-like shock seemed sensible.

Election night and the early morning hours the following day proved the polls wrong. Trump won handily, and market fears dissolved.

New policies and potential impacts

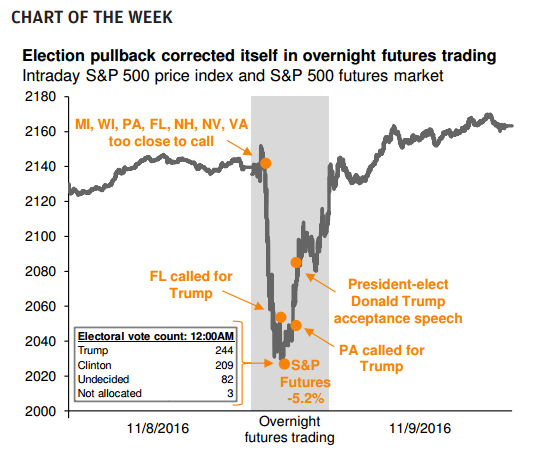

There was a shock in overnight trading of stock futures on election night. The S&P 500 was down 5% in a very swift move. It looked like markets were set to have a bad day the morning after the election, but stocks traded flat at the open and then rallied higher that day … and continued on an upward trajectory for most of November. The Brexit sell-off lasted two trading days; the market reaction to President-elect Trump lasted all of a couple of hours. It was a fascinating turn of events, and it now removes some of the uncertainty that has been weighing down markets and kept them largely range bound since July.

The overall market trend for 2016 is now optimistic based on expected policy reforms, and there are two major stimuli involved: tax reform and deregulation. Trump’s tax plan looks like it could be especially beneficial for businesses as corporate taxes could be cut by more than half, down from 35% to 15%. In addition, tax reform could influence U.S. businesses to repatriate billions in foreign revenues at a rather friendly 10% tax rate. Reduced corporate taxes will boost bottom line earnings, and repatriated cash could boost capital expenditures, stock buybacks, and dividends paid out to shareholders. All three of those could be a great boon to both the economy and investors.

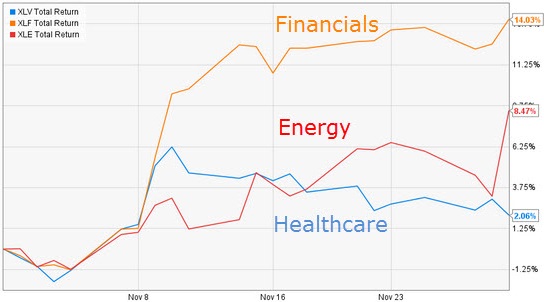

Put in simple terms, deregulation translates to a business-friendly environment, and initially it looks like that could be very positive for financial, healthcare, and energy companies. Trump has pledged to overhaul the Dodd-Frank Act, which was in large part enacted as a reaction to the Financial Crisis. Dodd-Frank compliance has proven to be burdensome to the financial industry, and the prospects of deregulation and higher interest rates have boosted the earnings expectations, and thus the stock prices of banks and financial firms. Trump has also vowed to repeal and replace the Affordable Care Act. The healthcare sector has traded lower most of this year with the expectation of a Clinton administration coming to power, but the charts (below) show a significant about-face in the healthcare sector after the election. Lastly, the energy sector is expected to benefit from a Trump administration as his views on energy and climate change differ greatly from those of the Obama administration. Sectors aside, Trump is viewed as pro-business and pro-growth, and the market trends in 2016 have moved in response to that.

Capital Markets and Interest Rates

U.S. stocks have performed very well since the election, but Developed International stocks, Emerging Markets stocks, and bonds have lost value. Domestic stocks in every market cap segment, from large-cap stocks down to small-cap stocks, ended November markedly higher, but mid-caps and small-caps had the strongest performance. That outperformance was due in large part to renewed interest rate expectations (discussed below) and the potential for the U.S. dollar to strengthen. The stocks of midsized and smaller U.S. companies outperformed their larger counterparts because these smaller companies are less influenced by currency issues. A strong U.S. dollar can be a headwind to large companies forced to export goods made more expensive by a surging greenback. Trump’s desire to repeal/revise the North American Free Trade Agreement (NAFTA) and his promise to withdraw from the Trans-Pacific Partnership (TPP) on his first day in office help explain the underperformance of international stocks. Some investment strategists claim that diversification is dead, but last month proves that it still works for investors and helps portfolios during times of greater uncertainty.

There was a major shift in interest rate expectations as a result of the election. The Federal Reserve Board has been very cautious in its interest rate policy, and that has amounted to only one, singular interest rate hike since the Financial Crisis began. The Fed has cited a myriad of issues for their slow and cautious approach: slack in jobs, lack of wage growth, low inflation, and even global conditions. Fed members have commented on Trump’s tax policy and fiscal spending as two factors which could send inflation higher; thus, the expectation of interest rate hikes has risen.

If you study Fed funds futures, you can get a sense of what the market expects. So, what’s the market’s assumption for a December Fed funds rate increase? The answer is about 99%. Market strategists and Fed watchers are now predicting multiple rate hikes in 2017, but that’s not really a surprise as they’ve predicted higher rates for more than five years now. However, conditions now seem more suitable for possible hikes in the near future.

Higher interest rates will be good for savers sitting on cash, which has provided them with very little income in recent memory. Higher rates will also be good for banks sitting on loan portfolios that have yielded little profits. And the combination of higher rates along with higher inflation could be good for real estate. But the path to higher interest rates has been a short-term shock to bond investors. Investment grade bonds had a terrific first half of 2016, as a lot of foreign money poured into U.S. bonds because their yields were higher than what could be found elsewhere. However, as interest rate hikes are now more likely, bonds have experienced some hefty outflows, and their values have taken a hit. In the two weeks following the election, roughly $10b moved out of bond funds, slashing the year-to-date return of those funds in half. The selling seems to be overdone though as the Fed funds rate still sits well below 1%, and probably won’t go over 2% until 2018. Everyone, including the markets, probably needs to just take a deep breath and see how Congress and President-Elect Trump work together after the inauguration in passing legislation regarding taxes, trade, healthcare, and so on.

A New Year, A New Deal

In September, members of the OPEC oil cartel tentatively agreed to production cuts in an effort to boost the price of crude oil. However, there was a lack of agreement on the details of the deal. OPEC held another meeting just last week that included several non-OPEC countries, and participants formally agreed to cut overall production by 1.2 million barrels a day. Oil prices and energy stocks rallied on the news.

The agreement is an interesting turn of events because it was on the Friday after Thanksgiving just two years ago, in 2014, when OPEC decided to make no changes to oil production. West Texas Crude had peaked in the summer of 2014 at around $107/barrel, and from June until November the price of oil plummeted by about -25%. The decision then to not cut or cap production was a strategy of allowing massive oversupply to send oil prices lower, a move intended to hurt frackers and shale players in the U.S. and drive some of them out of business. You might recall in past newsletters that we’ve highlighted how a weak U.S. energy sector has been a drag on overall S&P 500 earnings, so there’s no question that OPEC’s strategy to inflict pain on U.S. producers was successful.

However, the plan also meant that OPEC would be hurting their own pocketbooks. Venezuela’s already reeling economy was further harmed by lower oil revenues and now flirts with economic and political ruin. Even Saudi Arabia had to cut subsidies and perks for citizens, and non-OPEC countries like Russia have struggled mightily as diminished oil revenues damage their already fragile economy as well.

OPEC’s latest efforts to manipulate the price of oil must be closely monitored. As the production cuts go into effect in January, it will be interesting to see how quickly U.S. frackers can bring production back online and profit from higher prices. Some energy analysts are predicting a brief move up in oil prices followed by yet another decline when supply increases. Supply and demand will continue to drive oil to some near-term equilibrium price, but higher interest rates in the U.S. could lead to more U.S. dollar strength which would apply downward pressure to oil prices because oil is priced in U.S dollars. There are a lot of variables in play here, and OPEC meets again in mid-2017. Stay tuned.

Looking Ahead

After the Brexit and Trump surprises, there is another important vote to be held very soon that could also affect global markets. Italy is holding a referendum on reforming its Constitution on December 4th, and Italian Prime Minister Matteo Renzi believes that constitutional reform is necessary to provide political stability and allow the Italian government to operate more efficiently. The reforms are also critical in order to stabilizing the country’s banks which are burdened with €200 billion in bad loans. A no-vote would result in shifting more power to Italian politicians who are in favor of Italy leaving the European Union. Some economists predict that to be the end of the Euro, an event which would have major repercussions for global trade.

As mentioned before, the Fed’s December meeting should result in a vote to push interest rates higher. The stock market trends in 2016 expect a hike, so it’s likely that higher rates are already priced into stocks. However, 2016 has been a year of big surprises, so who knows for sure? Remember, this was the year that ended the Chicago Cubs’ “Curse of the Billy Goat” in the most dramatic of fashions. Cubs’ fans went from the agony of losing the first three games of the World Series to the ecstasy of winning the series’ final four straight games, breaking their 108-year-old year drought as Major League Baseball’s victor. The “Back to the Future II” film was only one year off in its prediction of a Cubs Championship, and on top of that Nike is making the film’s self-tying shoes a reality. Get ready to open your wallet though: a pair of the futuristic Nike HyperAdapt shoes will cost you a cool $720.