You know it’s the fall in North Texas when your kid comes home from school with tickets to the State Fair of Texas. The Fair just kicked off its 130th year, and it’s a pretty big deal in these parts with a number of attractions drawing hundreds of thousands of people every year. The State Fair of Texas is the biggest state fair in the country. Of course, right? The usual suspects are there: the rides at the midway, games run by the carnies, musical acts of all sorts, a car show, and an over-the-top fried food recipe contest. The Texas Longhorns and the Oklahoma Sooners football teams battle each other every year at the Fair Park grounds in the historic Cotton Bowl stadium, which just adds that much more excitement to the festivities. And of course, there’s the iconic Big Tex statue that greets fair-goers near the main entrance. The fair is almost always a fun diversion from the routine, but for many, it’s also a sign that the seasons are in transition – the hot Texas summer is over, and fall is upon us.

ECONOMIC EXTENSION

It seems like a lot of people are waiting for the economic cycle to transition from expansionary to recessionary, but the signs aren’t necessarily there yet. Yes, this current expansion cycle is long in the tooth, as is the current bull market. Yes, GDP continues to move at a snail’s pace. In fact, the U.S. Commerce Department recently released its final estimate of Q2 GDP and it came in at only +1.4%. That’s not much growth, folks. Also, housing starts and building permits ticked down in recent data releases. While this data can be a little concerning, there are also positive data points that give reason for mild optimism.

Non-farm payrolls increased by 151,000 in August, and the unemployment rate remained at 4.9%, a number almost any policy-maker would be happy with. Consumer confidence climbed to a post-crisis high in September, and gains in real consumer spending have averaged 3% since mid-2013. Household debt as a share of disposable income has also fallen to its lowest level since 2002. Help has come in the form of falling food and commodity prices—which have their own list of pros and cons—and many of these points support the consensus view that spending and GDP growth should continue to improve throughout the second half of the year. Economic data will most likely continue to disappoint in providing a clear picture of where the U.S. stands, but most economists put the risk of recession below 20%.

Abroad, the picture is more easily described as “improving.” Keep in mind that much of the developed world’s recovery from ’08-‘09 is several years behind the recovery we’ve seen in the U.S. Foreign central bankers adopted a “wait-and-see” approach to stimulus after the financial crisis, while the U.S. policy-makers jumped in with both feet to stem the economic carnage. More on that in a moment, but for now Eurozone GDP has stayed positive with the most recently released estimate for Q2 at a pretty meager 0.3%. Also positive was that a recent gauge of U.K. services provided evidence of an economic rebound from the shock the markets experienced on the heels of the surprise Brexit vote outcome. China released data in September showing a 6.3% increase in industrial output and a 10.6% increase in retail sales. However, recent warnings of excessive credit growth have made waves for the world’s second largest economy. Japan’s economy continues to struggle to find growth, but annualized GDP growth remains positive at 0.7% – not great, but at least they’re keeping their heads above water.

The counter-argument for a positive international outlook continues to focus on commodity-centric countries, especially the major oil producers like Venezuela, Russia and Saudi Arabia. Venezuela remains in absolute crisis, and Russia’s central bank cut interest rates by 0.5% in an attempt to tamp down inflation. Saudi Arabia continues to grapple with depressed revenues due to low oil prices. The salaries of Saudi government workers have been slashed by 20%, and many financial perks for public sector employees have been scaled back. Pay cuts are expected to affect two-thirds of Saudi workers all told. And, last month the World Trade Organization cut its forecast for global trade growth by a third, down from 2.8% to 1.7%. That’s pretty big …. like Big Tex big.

CENTRAL BANKING

At the beginning of September, a few Federal Reserve presidents were quoted voicing comments that most observers would view as hawkish. Many of these comments followed the annual economic symposium in Jackson Hole, Wyoming, where the focus was around monetary policy and how to use it to cope with economic stresses going forward. With the Fed and possible rate hikes on the minds of market participants, U.S. stocks started the month heading lower. It seemed that, once again, the Fed was messaging a rate hike, but when the September 20th-21st meetings came and went, no rate hike materialized. So stocks rallied. Maybe we’ll get a small rate hike in December, but let’s all remember that back in late 2015, the Fed was trying to sell us on the idea of four rate hikes this year. Like Big Tex, it appears there’s a whole lot of loud talk and not much action.

Global central bankers and finance ministers also delivered a similar message in a G20 joint communique early in September: “We are determined to use all policy tools – monetary, fiscal, and structural – individually and collectively to achieve our goal of strong, sustainable, balanced and inclusive growth.” A few days after issuing that statement, the European Central Bank chose to leave rates and stimulus policies unchanged. However, late in September, the Bank of Japan announced major changes to its monetary policy framework, and may ultimately implement something like “QE infinity” – a policy of buying Japanese government bonds forever. Also of note is that Saudi Arabia pumped about $5b of capital into its banking system. It seems nothing helps inoculate markets from crises like some good old fashioned liquidity.

To summarize, no central bank for a major economy is presently tightening monetary policy. The policies for all of the major players remain in favor of continued attempts to stimulate growth. Interest rates remain historically low around the world, and they are actually negative in some markets. Investors in search of income and growth continue to be nudged towards risk assets like stocks and real estate. The S&P 500 finished the month exactly flat for the month; the Barclay’s Capital Aggregate Bond Index was down -0.1%; the MSCI Developed EAFE finished up 1.3%, and the MSCI Emerging Markets Index also finished up 1.1% for the month of September.

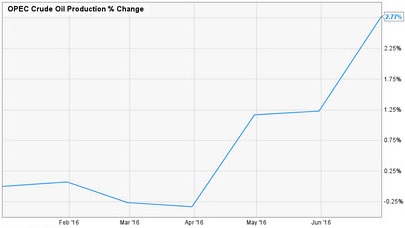

OPEC OIL DEAL

If meetings and policy announcements from the Fed, the European Central Bank, and the Bank of Japan were not enough, another meeting made headlines as September came to a close. OPEC members met in Algiers to discuss production, and it appears that an agreement is now in place for modest oil output cuts. However, how much each country will produce is to be decided at the next formal OPEC meeting in November, when an invitation to join cuts could also be extended to non-OPEC countries like Russia. The price of oil jumped 5% on the news, and the ripple effects extend obviously to oil producers and maybe not so obviously to the credit markets. Energy sector-related debt makes up about 14% of below-investment-grade bonds, and the risk of waves of defaults by bonds tied to energy firms have eased for now. We’ll have to see how this plays out as fracking technology can bring production back online pretty quickly, so attempts by OPEC to balance production may be countered by U.S. frackers looking to improve their cash-flow statements.

Another chapter is coming to a close soon. In a little over a month, the U.S. will decide on its next President. The first presidential debate attracted a historic audience, both on live TV and in live streams online. The market’s consensus view is that a Hillary Clinton presidency is a continuation of current policy for the most part. Traders know what that means and seemed to give her the nod after the first debate as stocks rallied to start the final week of September. A Donald Trump presidency is less clear in terms of policy implications, and since markets generally dislike uncertainty, a close race or a win by the Republican would likely mean more volatility and maybe a market sell-off until things settled out. A positive similarity between both Clinton and Trump is that both candidates favor additional infrastructure spending, which could be good for jobs and the economy, at least in the short and medium term.

The coming debates will almost undoubtedly contribute to market volatility in the short term, and no matter who you plan to vote for, just remember that there’s a big difference between what’s promised on the campaign trail and what actually gets done in real life. Comparisons have already been drawn between the U.S. presidential election and the Brexit vote, and those comparisons make sense in many ways as they apply to capital markets. Votes cast across the U.S. will be counted in a single day for election outcomes, but policies and legislation will take weeks, months, and sometimes years to implement and then impact the world around us. As it translates to the capital markets, it stands to reason that the most attractive stocks, bonds, and real assets may be those right here in America.