The federal government spent $4.8 trillion in 2019. That’s $150,880 per second, but it gets worse. In the plague year of 2020, it spent $6.8 trillion, which comes to … oh, who cares? It’s a lot and it’s bound to be even higher this year, especially with at least another round or two of pandemic relief coming our way.

And none of this would be an issue, except that a big chunk of it is borrowed money. The budget deficit – what the government spends in excess of what it brings in via taxes and fees – ballooned from $85.2 billion in 2019 to $279.0 billion during Hell Year.

And even this wouldn’t be an issue, except that current federal deficits aren’t one-off things. With the exception of the dotcom- and “peace dividend”-fueled years of Bill Clinton’s second term, there hasn’t been such a thing in our adult lives as a federal budget surplus. These current federal deficits have accumulated to the point that the total deficit is approaching $27 trillion. That’s four 2020s, and somebody’s going to have to pay for it, either us or our children or our grandchildren.

The received wisdom is that all this debt will make bond buyers loathe to lend more money to Washington, leading to higher interest rates, which in turn will fuel debt and inflation. Every expert, it seems, is predicting an impending bout of inflation which will rob us all of our lives’ savings, render the dollar nearly worthless and turn America into Venezuela.

No need to rehash all that now, but a fair question is: Why hasn’t it happened yet? What’s keeping inflation under 2% — at least so far? Why aren’t we insisting on getting paid every day to stay ahead of the cost of living? When we go to the supermarket, how come a stocker isn’t repricing the bread, milk and eggs we already have in our carts?

Another question is: How long can our luck hold out?

Why we should be worried

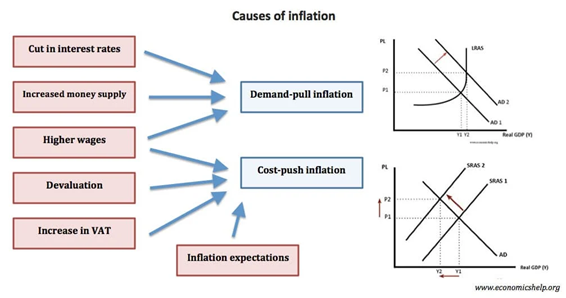

According to Oxford University economist Tejvan Pettinger, there are six causes of inflation:

- Cut in interest rates,

- Increased money supply,

- Higher wages,

- Devaluation,

- Increase in taxes, and

- Inflation expectations.

So, let’s go through Pettinger’s list. Cut in interest rates? Check. Even before Washington displayed any observable medical response to the pandemic, it kicked into gear on the economic response. The Federal Reserve reduced target interest rates to near-zero as early as March 15, 2020 – and how often do central bank governors work on a Sunday?

Increased money supply? Check. Immediately after lowering interest rates, the Fed flooded the economy with new dollars. M2, the most widely cited measure of how much money is in circulation, had been inching up for years but 2020 saw it go from $15.5 trillion to $19.3 trillion. That’s a 25% jump.

Devaluation? Check. The greenback lost almost 5% against a market basket of currencies in 2020, but Citigroup foreign exchange strategist Calvin Tse is bracing his clients for a drop of up to another 20% over a multiyear period. His thesis is that this cyclical downturn was already in the works when the economy locked down so, as soon as we reemerge from our Covid chrysalis, we should anticipate that shift with all due pent-up force.

Which brings us to expectations. There is hardly an economist in the world who’ll tell you that inflation in 2021 will be close to 0%. They all agree debt and inflation are coming, and they can’t agree on where to go for lunch.

Why we shouldn’t panic

But what about those drivers we didn’t check off?

Increased taxes? Not on Donald Trump’s watch. It’s bound to happen under Joe Biden’s, but there’s been nothing concrete on that yet. We’ll discuss this more in the column below. Still, it’s hard to imagine the magnitude of a tax hike that would trigger inflation when zeroing out the Fed funds rate and turning the sky green with newly printed dollar bills fails to do so.

Higher wages? Again, not on Trump’s watch – but not on Obama’s, Bush 43’s, Clinton’s, Bush 41’s … all the way back to Johnson’s. The Pew Research Center found that, as of 2018, real hourly wages have “hardly budged”. That is, paychecks have more or less kept pace with inflation, but they’ve likely had little to do with fueling it.

Further, there’s a lot of revisionist thinking around the effects of interest rates and money supply. To start with, the effective Fed funds rate was already low before the pandemic. It peaked at 2.4% briefly in mid-2019 after years of flatlining near 0% and has generally been in the single digits every day since 1984. We have a lot of room to run before it hits the all-time high from 1981 of 17.79%. And as harsh as lending terms were in the mid-1970s through the mid-‘80s, inflation in that period never exceeded 14.8% which, while high, isn’t Venezuela-Zimbabwe-Weimar Republic high.

And let’s remember that no raw number, as big as it might be, should be seen as some kind of scary monster. It’s important to keep your eye on the ratios – how big it is in terms of something else. Being $100,000 in debt might be crippling to a recent college graduate, yet an established dental surgeon might call it “my total car loans.” By the same token, America’s $27 trillion federal debt needs to be compared to the roughly $21 trillion of economic activity the country generates in a year. If we can individually pay off mortgages of quadruple our annual income, perhaps we can in the aggregate afford to carry a debt burden of 1.3x gross domestic product. And when you compare the additional $3.8 trillion in 2020-vintage new money to that $21 trillion GDP figure, it doesn’t exactly fade into insignificance, but at least it’s a little less nerve-jangling.

All that said, persistent deficits do lead to growing debt. Debt must be paid back and, as long as interest rates stay this low that’s not a problem. But debt can spike and, when it does, there will be a reckoning. It’s coming, but there’s no telling when.

If we had to guess, though, it’ll hit us like a bludgeon when our backs are turned. We knew there’d be one someday but, when the pandemic hit, it came out of nowhere. There were warning signs for years but, when it finally came to pass in 2008, the financial meltdown came out of nowhere. When inflation comes, then, it might arrive all at once while we’re focused on some other “existential threat.” How prepared are you to hedge against high debt and inflation when that day comes? If you don’t know, then maybe it’s time to consult a qualified financial professional.