According to traditional etymology, the month of April derives its name from the Latin verb aperire which means “to open”. This makes sense as April is known as the month when trees and flowers begin to bloom in earnest.

The blooming that dominated this April 2016 economy involved geopolitics as much as horticulture, however. Tensions were high in Syria and North Korea at mid-month, which proved a negative catalyst for global equity markets. Investors bolted for safer havens like bonds, driving bond prices sharply higher while sending yields lower. Later in April, financial markets welcomed the results from the French presidential election’s initial ballot, where the self-avowed centrist candidate Emmanuel Macron survived to face far-right candidate Marine Le Pen in the run-off election in early May. The result sent the French stock market higher by 4.1%. US and European stock markets also rallied on the news. Near month-end, President Trump surprised the markets when he slapped levies of up to 24% on softwood lumber imports from Canada. Many analysts see the imposition of tariffs as the administration’s way of setting the tone ahead of talks on reforming the North American Free Trade Agreement (NAFTA). Amidst all of the missile launching, politicking and tariff imposing, the global stock markets found a way to blossom into positive territory by month-end. In fact, the late month surge helped the S&P 500 post its sixth monthly gain in a row.

US STOCKS

US stocks lost value in the first two weeks of April, before slowly beginning to turn things around mid-month. Optimism about first-quarter earnings results alleviated concerns over geopolitical risks, and US Treasury Secretary Steven Mnuchin announced that the Trump administration expected to release a tax reform proposal, an announcement which was well-received by investors. Major US stock indexes rose around 2%, and the S&P 500 climbed to within 0.5% of its record high set on March 1, 2017. The final week of April saw the NASDAQ Composite index close above 6,000 for the first time. Even with what looks to be an improving earnings picture, stock market valuations have a lot of investors concerned. Consider that according to FactSet, companies in the S&P 500 have traded at more than 20 times their past 12 months of earnings for 106 consecutive daily trading sessions. That’s the longest such stretch since 2010.

US EARNINGS

Heading into the first quarter’s earnings season, the consensus among analysts was that the earnings of companies in the S&P 500 would rise around 9% compared with the same quarter a year ago. Disappointing earnings results from a handful of big companies weighed on stocks at times during the month, but a flurry of strong earnings reports helped lift stocks in late April. So far in this earnings season, with only about half of the S&P 500 companies reporting to date, aggregate earnings are on track to rise more than 12.4% from Q1 2016.

US ECONOMY

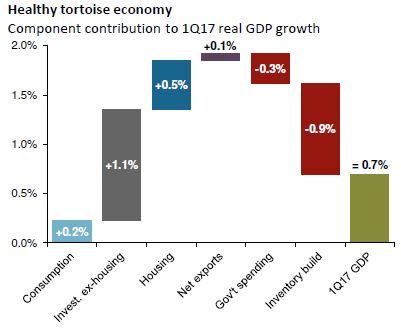

The US April 2016 economy got off to a sluggish start in the first quarter, with GDP growing just 0.7%, the weakest quarter of growth in three years. Deceleration in consumption and slower-growing inventories were the two main reasons for weak growth. However, a gauge of US consumer sentiment rose again in April, extending a climb that started after the presidential election last November. Also worth being mentioned, first quarter GDP got a boost from a meaningful pickup in investment spending, which is an encouraging sign for future growth.

FOREIGN MARKETS

Outside of the US, the world’s larger economies appear to be growing as well. Export growth in China accelerated in March, a positive sign for global demand. Economic growth in Europe is picking up after a long period of slow progress, according to recent survey results. Manufacturing business activity in the Eurozone jumped in April to a six-year high. Of the eight nations covered in the survey, only Greece failed to show signs of improvement. Overall, this relative surge in activity should make a significant contribution to overall economic growth on the continent. Global equities staged a relief rally after Macron advanced to the final round of the French presidential elections, where he’ll square off with Le Pen. Macron holds a 20-point lead in the polls ahead of 7 May’s vote. The post-French election rally lifted the MSCI World Index to an all-time high during the last week of April.

CENTRAL BANKS

Minutes released from the March meeting of the US Federal Reserve Board’s confirm that the Fed plans to continue tightening monetary policy by raising the fed funds rate again later this year. However, the Fed is expected to keep interest rates unchanged when it concludes a two-day meeting to be held the first week of May. Some Fed watchers think the Fed may pause in raising rates for several months due to the recent slump in US GDP, but the Fed will likely feel compelled to continue tightening sooner as there are signs that inflation is building. The Fed also wants to reduce the size of the agency’s $4.5 trillion portfolio of U.S. Treasury and mortgage-backed securities accumulated over the years in the wake of the Great Recession as well. In contrast to the US, the European Central Bank (ECB) and the Bank of Japan (BOJ) are sticking to their loose to ultra-loose monetary policies. ECB President Mario Draghi acknowledged that downside economic risks have diminished in Europe but offered no hints as to if or when the ECB will begin to dial back its asset purchases. In Japan, the BOJ indicated it will maintain its present ultra-loose monetary policy amid signs of slightly stronger domestic growth yet still-very-low inflation.

FINAL THOUGHTS: DEMOGRAPHICS ARE DESTINY

While it’s natural to track the day-to-day, week-to-week, quarterly and annual happenings in the world markets, sometimes it’s helpful to pull way back and look at the big picture: what big things are the real drivers of the markets – of societies, even – long-term? One of the biggest influences on the future has always been demographics, and we are living in the midst of a major shift in demography that is without precedent in human history. The people living in the developed markets and China will see their populations age rapidly in the coming years, and it’s going to impact virtually everything.

Bruce Wolfe and Russ Koessterich at Blackrock point out that the aging of our populations contribute to the economic environment in two big ways: it drives down economic growth, and it suppresses interest rates. These forces are problematic for politicians and policymakers whose goals are to drive up economic growth and facilitate environments where capital is rewarded with suitable returns. At its most basic level, economic growth is derived from a labor force making things and delivering services to others. Since our populations are beginning to skew older, and older individuals work less on average, all other things equal, our labor force will have fewer participants, meaning fewer goods and services.

The graying of China and much of the developed world also contribute to lower interest rates. Older people borrow less and save more. They tend to invest in safer asset classes and favor assets that throw off income, which means there will be an increased demand for bonds. Increased demand will mean less supply. Less supply will mean scarcity and higher prices. Higher bond prices will drive yields lower. And lower yields will mean lower interest rates in general. A lot to think about and some big problems to solve, but the markets seem to find a way to sort out a lot of these things themselves. Statistics show that the retirement savings set aside by older Americans are woefully insufficient for most of them. Since they’ll be living longer and will remain healthier longer than any previous generation in human history, it may become apparent that working longer is both necessary and personally fulfilling. The truth is the world’s developed countries need their older workers to stay engaged in the workforce. Maybe hard work pays off after all and keeps paying off. We’ll see …