Albert Camus, the French philosopher and author who won the Nobel Prize in Literature in 1957, probably had October on his mind when he wrote: “Autumn is a second spring when every leaf is a flower.” Camus died in January of 1960, so his last October among the living was in 1959. If he’d have been alive for this year’s version of October, it’s unlikely the beauty and wonder of the fall foliage would have been on his mind.

This October has been dominated by major headlines around the world, but the most prominent ongoing news story has been a U.S. election season. It’s unlike anything our country has ever seen before.  There have been vicious personal jabs by both candidates – Hillary Clinton and Donald Trump – and leaked emails appear to incriminate Clinton and other Democrats secretly conspiring to manipulate the outcomes of all sorts of things. There are the allegations of past sexual misconduct by Trump, countered by his recounts of Bill Clinton’s improprieties, not to mention the pay-for-play schemes and the charges of allowing foreign governments to tamper with our elections. According to the polls and odds-makers, Clinton was still a heavy favorite toward the end of October, with a 5 to 1 chance of beating Trump. Now those odds are down to 3 to 1 and Trump is gaining momentum, due in large part to the FBI’s discovery last week of several thousand more previously undisclosed Clinton emails the subject of prior investigation. Trump’s rallies have always been larger and more enthusiastic than Clinton’s, so in some ways the polling data just doesn’t add up. But maybe the polls are right and Clinton will win Florida and the election early in the evening next Tuesday, and we can turn the TV off and go to bed earlier than we thought. Then again, it could get really interesting if battle ground states break for Trump. We’ll just have to wait and see.

There have been vicious personal jabs by both candidates – Hillary Clinton and Donald Trump – and leaked emails appear to incriminate Clinton and other Democrats secretly conspiring to manipulate the outcomes of all sorts of things. There are the allegations of past sexual misconduct by Trump, countered by his recounts of Bill Clinton’s improprieties, not to mention the pay-for-play schemes and the charges of allowing foreign governments to tamper with our elections. According to the polls and odds-makers, Clinton was still a heavy favorite toward the end of October, with a 5 to 1 chance of beating Trump. Now those odds are down to 3 to 1 and Trump is gaining momentum, due in large part to the FBI’s discovery last week of several thousand more previously undisclosed Clinton emails the subject of prior investigation. Trump’s rallies have always been larger and more enthusiastic than Clinton’s, so in some ways the polling data just doesn’t add up. But maybe the polls are right and Clinton will win Florida and the election early in the evening next Tuesday, and we can turn the TV off and go to bed earlier than we thought. Then again, it could get really interesting if battle ground states break for Trump. We’ll just have to wait and see.

In any case, the 2016 U.S. election speaks to a problem that’s going on here in the U.S., and around the world as well. Trump’s popularity, and that of former Democratic Presidential hopeful Bernie Sanders, stems in large part from the frustration of the middle class with the establishment and the status quo. This election cycle may be looked back on as having fundamentally changed both of America’s major political parties. And the angst that drives the change is the same sort of anger and frustration that led to the unexpected Brexit referendum outcome only a few months ago in which U.K. voters surprisingly chose to exit the European Union.

Monetary policy and economic news

With the 2016 U.S. election looming on November 8th, the U.S. Federal Reserve Board is not expected to take action on interest rates when it concludes a two-day meeting on November 2nd. In fact, the Fed has raised short-term rates only one time in the last 40 years in the three-month period preceding Election Day. However, the Fed’s policy statement from the meeting should be closely watched for clues about what policymakers think about a possible rate increase in December. Many Fed members think that a rate increase is overdue and that rates have been too low for too long, which they fear has distorted asset prices. Other Fed members fear raising the fed funds rate too soon, which they claim could throw a very slow-growing U.S. economy into recession.

Recent economic data has been mixed. The U.S. economy grew at a 2.9% annualized pace in the third quarter, the fastest pace in two years, and a marked improvement from the first half of the year when GDP plodded along at closer to 1%. However, the composition of the third quarter’s gain was slightly unfavorable, with more inventory accumulation and less final sales growth. Inflation in the U.S. is showing signs of stirring, though it remains below the Fed target. Core inflation reached a two-year high of 1.7% last quarter, while wages rose 2.4%. However, consumer confidence declined by more than expected in October, reflecting a fall in both consumers’ assessment of their present situation and their forward-looking expectations.

Across the Atlantic, European Central Bank (ECB) President Mario Draghi signaled in October that policymakers may extend their bond-buying program beyond March 2017, when the ECB’s quantitative easing program is scheduled to end. Eurozone economic growth remained steady at a paltry 0.3% in Q3, and has increased 1.6% over the past year, suggesting the bloc’s steady recovery has not so far been knocked off course by Britain’s vote to leave the EU. Speaking of which, the British economy grew by a much better-than-expected 0.5% in the third quarter, the first time period for which impacts from the Brexit vote could fully be analyzed. Initial predictions of doom post-Brexit have yet to materialize – with the exception of the crashing pound – and economic data has broadly held up well.

Things in Japan aren’t going as well. Bank of Japan (BOJ) Governor Kuroda said recently that the BOJ may once again push back its 2% inflation target, which currently sits somewhere in fiscal 2017. Recall that when he started his job in early 2013, Kuroda kicked off his turbo-charged asset purchase policy that continues to this day, and he had hoped that inflation would hit 2% by late 2014 or 2015. Almost four years later, inflation has vanished after an initial rise. Japan’s industrial output was unchanged in September, falling short of forecasts, in a worrying sign for the economy as the BOJ board gathers yet again to consider monetary policy changes. In China, remarkably steady growth rates for three straight quarters has some economists suspicious, but the country’s state media agency claims that Beijing is not “data smoothing” its GDP numbers. Separately, China’s industrial profit growth slowed in September as several sectors showed weak activity, but recent Purchasing Manager Index data is stronger. Again, mixed signals abound. Among emerging markets, India is a country on the rise. India’s economy is forecasted to grow by +7.6% in calendar year 2017, a result that would make it the fastest-growing major economy in the world for the 3rd straight year.

Capital markets

Stocks in the U.S. as well as in the world’s developed and emerging markets all slid in October. U.S. and developed market stocks fell about 2%, while emerging market stocks slipped only about 1%. The S&P 500 still sits about 3% below its record high reached in mid-August. For the year, the U.S. and the developed markets are up around 5% and 4%, respectively, while emerging market stocks are up almost 15%. Bonds are up 3% for the year, but were down 1% in October, as the recent uptick in inflation has dampened returns. The yield on the U.S. 10-year Treasury bond spiked recently to its highest level in five months (yields move inversely to prices), but yields still remain near historic lows. In fact, last Friday (10/28) marked the 190th consecutive trading day that the 10-year Treasury has closed with a yield below 2%, the longest stretch below 2% in history. 10-year notes have traded in the U.S. since 1790.

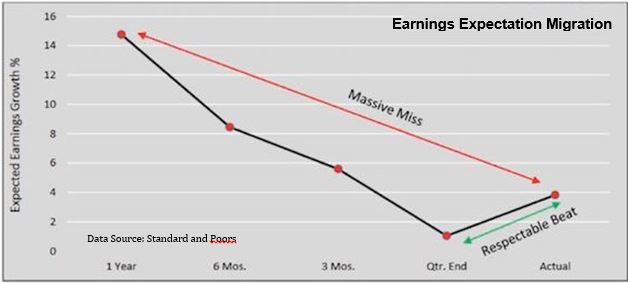

For the third quarter, the blended (combines actual results for companies that have reported and estimated results for companies yet to report) earnings growth rate for the S&P 500 is 1.6%. It’s still hard to say whether overall earnings for the third quarter will post a slight gain or will decline for the sixth consecutive quarter. In any case, it’s unfortunate that, in many ways, U.S. corporate earnings has evolved into a giant expectations shell game. You can see the problem all the time in the way analysts, in response to a company’s guidance, revise their forecasts downward as the release of the earnings report approaches. These are averages for the 17 quarters from 2Q 2012 through 2Q 2016: Profit projections made one year out are usually way too optimistic. Over the next twelve months they fall steadily to a point just below the eventual actual number. Voila: a huge failure to deliver on the year’s goal gets transformed into a “we beat expectations” victory.

For the third quarter, the blended (combines actual results for companies that have reported and estimated results for companies yet to report) earnings growth rate for the S&P 500 is 1.6%. It’s still hard to say whether overall earnings for the third quarter will post a slight gain or will decline for the sixth consecutive quarter. In any case, it’s unfortunate that, in many ways, U.S. corporate earnings has evolved into a giant expectations shell game. You can see the problem all the time in the way analysts, in response to a company’s guidance, revise their forecasts downward as the release of the earnings report approaches. These are averages for the 17 quarters from 2Q 2012 through 2Q 2016: Profit projections made one year out are usually way too optimistic. Over the next twelve months they fall steadily to a point just below the eventual actual number. Voila: a huge failure to deliver on the year’s goal gets transformed into a “we beat expectations” victory.

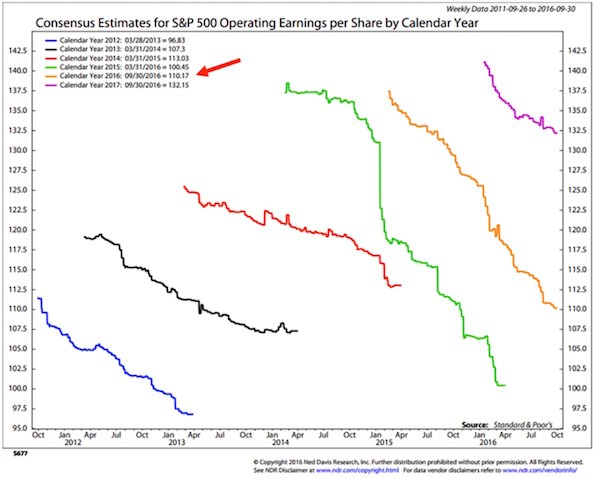

This chart shows how this phenomenon works itself out over several years of data. The chart starts  with the year 2012, and there has not been one year since that has not seen a significant revision downward of earnings forecasts. Note that initial estimates have been higher every year than the year before, except in 2016, and that the drop-off in earnings estimates was more precipitous in 2015 and 2016 than in prior years. In 2015, consensus estimates went from an initial forecast of $137 to barely above $100 by the end of the year. That is a huge miss – over 30%. But that expectations dive didn’t dismay the analysts, because they initially predicted roughly the same level of earnings for 2016; and as of September 30, it looked as though earnings are going to come in at roughly $110. For 2017, earnings predictions started above $140 and are now down to $132. In a world where GDP growth may be in the neighborhood of 2%, does it really seem likely that earnings are going to grow by 20% in 2017?

with the year 2012, and there has not been one year since that has not seen a significant revision downward of earnings forecasts. Note that initial estimates have been higher every year than the year before, except in 2016, and that the drop-off in earnings estimates was more precipitous in 2015 and 2016 than in prior years. In 2015, consensus estimates went from an initial forecast of $137 to barely above $100 by the end of the year. That is a huge miss – over 30%. But that expectations dive didn’t dismay the analysts, because they initially predicted roughly the same level of earnings for 2016; and as of September 30, it looked as though earnings are going to come in at roughly $110. For 2017, earnings predictions started above $140 and are now down to $132. In a world where GDP growth may be in the neighborhood of 2%, does it really seem likely that earnings are going to grow by 20% in 2017?

Commodities – assets you can hold in your hands – are having a good run as of late. For the first time since June, crude oil prices climbed above $50 a barrel in early October, but they’ve given back some value since then. Still, oil prices are up more than 30% for the year so far. Gold is also up markedly year-to-date, having appreciated almost 20% for the year. Silver is also up substantially, posting a gain of almost 30% for the year. Precious metals are seen as a safe haven in a crisis, so they tend to appreciate when investors are fearful.

Summary

The seasons, the markets, and political elections here and around the world all show us that the one constant in our world that we can count on is change. We spoke a few months ago about technology innovations that are coming, including autonomously driven vehicles. Many tech experts say that self-driving trucks will be the first wave of vehicles that we’ll see on the road because of high demand for the technology. Logistics firms just can’t find enough drivers to man their routes and traditionally driven vehicles can only be operated for 11 hours at a stretch. In a major milestone for autonomous trucking, some 45,000 cans of Budweiser beer arrived recently at a Colorado warehouse after traveling more than 120 highway miles in a self-driving semi with no driver at the wheel. The driver monitored the truck’s activity from the sleeper berth for the entire two-hour journey. Another application of driverless technology is “platooning”. Here, a lead truck has a human driver and leads a “road train” of several other trucks with empty cabs programmed to follow the leader.

Another change we’re seeing here in the U.S. is the legalized consumption of recreational marijuana. The issue is on the ballot this month in five states: Arizona, California, Maine, Massachusetts and Nevada. Recreational marijuana usage is already legal in four states: Colorado, Washington, Oregon and Alaska, plus the District of Columbia. If the issues pass in all five states, then 23% of U.S. citizens will live in a state where recreational marijuana usage is legal. If there’s anything worse than being passed by an 18-wheeler barreling down the highway and driven by a stoned trucker, it would be realizing that same trucker has 4 driverless trucks “platooning” behind him and following his every lead. Now that’s a convoy I’d just let roll on by ….

The issue is on the ballot this month in five states: Arizona, California, Maine, Massachusetts and Nevada. Recreational marijuana usage is already legal in four states: Colorado, Washington, Oregon and Alaska, plus the District of Columbia. If the issues pass in all five states, then 23% of U.S. citizens will live in a state where recreational marijuana usage is legal. If there’s anything worse than being passed by an 18-wheeler barreling down the highway and driven by a stoned trucker, it would be realizing that same trucker has 4 driverless trucks “platooning” behind him and following his every lead. Now that’s a convoy I’d just let roll on by ….