As Chinese New Year celebrations wind down, it’s fitting to recall an expression that has been attributed to the Chinese for generations. The expression “May you live in interesting times” has an origin that is, ironically, interesting itself. Regardless of its origin, upon closer examination, the expression seems not to be a blessing at all, but a curse. ‘Interesting times’ have historically been associated with periods of disorder and conflict while ‘uninteresting times’ typify periods of peace and prosperity. Blessing or curse, few would say that the world today is ‘uninteresting,’ and one of the most interesting things going on in the world right now has been the unfolding repudiation of the establishment class by the electorate in the U.S. as well as in other Western democracies.

WHAT HONEYMOON?

Love him or hate him, the world’s largest superpower only a few months ago elected a billionaire businessman and television personality to the highest office in the land. President Trump is also the oldest and wealthiest person elected to the office in the nation’s history and the first without prior military or governmental service to his credit. He rode to victory on a platform focused on populist themes like renegotiating trade deals, repealing and replacing Obamacare, reducing regulation in an effort to help U.S. businesses and workers, enforcing federal immigration laws, pursuing energy independence, and investing substantially more in infrastructure projects and national defense. President Trump has encountered strong and energized resistance since the first day he assumed the office, but with Republican majorities in both houses of Congress, he will have the opportunity to usher in a period of sweeping policy change in America.

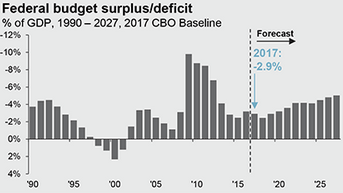

Be assured that most of these changes will impact the investment environment. However, the changes that occur will be influenced significantly by political, ideological, and economic realities, not to mention other players including the Federal Reserve and our trading partners. For example, President Trump has proposed both tax cuts and increased infrastructure spending, both of which would add to the deficit in the face of rising interest rates. Even Congressional Republicans may not be on board with adopting these measures as proposed. They may point to recently released data by the Congressional Budget Office (CBO) showing that, in percentage terms, our national debt is growing faster than our economic output and that even without any policy changes the federal budget deficit will increase relative to gross domestic product (GDP) due to increased Social Security outlays and growing interest payments on our national debt. Trump contends that his policies make 4% economic growth a possibility. The CBO projects 2% growth based on current policies. Neither is likely correct. The origin of the expression “only time will tell” is officially unknown, so for all we know it may be Chinese. If not, maybe it should be.

STOCKS

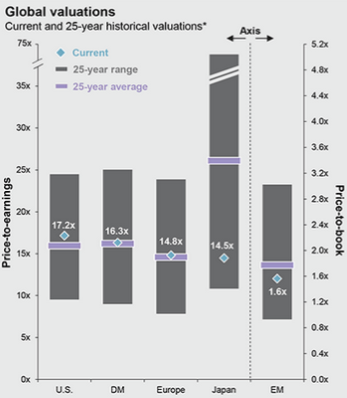

The Standard & Poors 500 (the S&P) hit an all-time record high in the first week of the new year, which portended a good month for stocks all around the world. The S&P went on to hit another record high later in January and finished the month up 1.9%. Since the November 8th election, the S&P is up more than 6%. Another U.S. stock market index, the Dow Jones Industrial Average (the Dow) made headlines in January as well. After hovering within a couple hundred points of 20,000 for several weeks, the Dow closed above that threshold for the first time on January 25th. The Dow’s ascent to 20,000 was a fast one, as it came just 42 trading days after the index crossed the 19,000-point level for the first time back in November. International markets fared even better than the U.S. did in January. Developed market stocks were up 2.9% in January while emerging market stocks surged more than 5.4%. The global stock market was up 2.6% for the month overall. While recent gains in stocks give investors reason to cheer, it would be wise to proceed with caution, as several market valuation metrics suggest that the U.S. stock market may be getting ahead of itself. Stock price-to-earnings multiples show the U.S. market is more expensive than its long-term average, and contrarian signals – like strategists’ and retail investor optimism, the 2016 year-end buying frenzy, and the discounting of headwinds like a strong U.S. dollar and the potential for protectionist policies — are all what you would expect to see around a major market top.

BONDS

The U.S. bond market recovered slightly in January after spending the final two months of 2016 in sharp decline. U.S. bonds were up only 0.2% for the month, but after tumbling almost 3% in November and December, a significant drop for the conservative asset class, anything above breakeven was welcomed. Rising expectations for a positive 2017 economic trend turnaround in Europe led to a sell-off in bonds there as well, causing German, French and Italian bond yields to hit highs not seen in years. (Bond yields move inversely to prices.) With interest rates likely to rise in the future, a diversified approach makes the most sense for investors who need exposure to fixed income assets.

ECONOMY

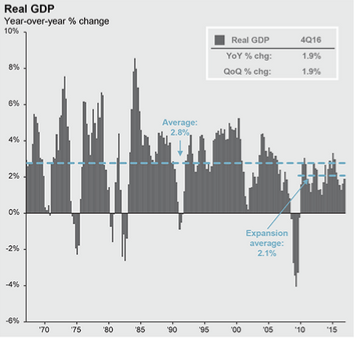

The U.S. economy ended 2016 on a slightly weaker note, with the Commerce Department’s first estimate of GDP for the fourth quarter showing growth slowing to an annual rate of 1.9%, from a third quarter annual rate of 3.5%. For all of 2016, the pace of expansion finished at 1.6%, the lowest annual rate in 5 years, and well off the 2.6% rate recorded in 2015. Employment growth has moderated recently as well. December’s gain of 156,000 jobs was below most economists’ expectations. However, 2017 economic trends show that wages are up 2.5% on a year-over-year basis, and the Institute for Supply Management’s monthly manufacturing index for the United States rose to its highest level in two years in December, so there’s good news out there as well.

In foreign markets, slow growth has also been a big theme. The European economy shows signs of growth as the Eurozone economy kept pace with the U.S. for the first time since 2008. Meanwhile, two of the world’s largest emerging market players – China and India – are experiencing a larger disparity of outcomes. China recently reported a slowdown in trade, with exports falling nearly 7.7% in 2016. The drop was the second annual decline in exports in a row, and the worst since 2009. In contrast, India has become more of a bright spot. India’s Finance Ministry forecasts that growth could dip to around 6.5% in the current fiscal year, before picking up to as much as 7.5% in the next fiscal year.

FED

As expected, the Fed kept policy rates unchanged following the central bank’s February 1st meeting. It was only at their last meeting in December that the Fed raised rates for the first time since late 2015. Federal Reserve Chair Janet Yellen said in a speech in January that most Fed officials expected to raise rates a few times each year through 2019. Rate increases are expected because the Fed sees inflation on the rise and is trying to stay out ahead of it. The Fed’s preferred measure of inflation, the Personal Consumption Expenditure (PCE) deflator, showed the core estimate growing 1.6% year-over-year for November, and other markets-based indicators of inflation are also picking up, suggesting a quicker pick up in prices soon.

CURRENCIES

The U.S. dollar has been on a wild ride versus a basket of other major currencies since the election last fall, and in January in particular. After climbing to its highest level in 14 years around the New Year holiday, the USD has fallen almost 2%, posting its worst start to a year in three decades. The drop may be due in part to comments President Trump made in a recent interview when he said the USD is “too strong” (versus other currencies). However, the greenback’s recent slide is small potatoes when compared to the Mexican peso, which has declined in value approximately 20% versus the USD since the U.S. elections.